How To Fill Out A Deposit Slip? A deposit slip is a document that specifies the particulars of a deposit made at a bank or other financial institution. The slip includes the date of the deposit, the name of the depositor, and the amount deposited. The deposit slip also records the account number of the account into which the funds are deposited.

In order to make a deposit at a bank, customers must complete a deposit slip specifying all pertinent information about the transaction. This includes the date of the deposit, the name of the depositor, and how much money is being deposited. The customer must also provide their account number to ensure that their funds are deposited into the correct account.

Deposit slips can be completed in person at a bank or online through an institution’s website. Customers often use online banking services to make deposits because it is more convenient than visiting a physical bank branch.

How To Fill Out A Deposit Slip?

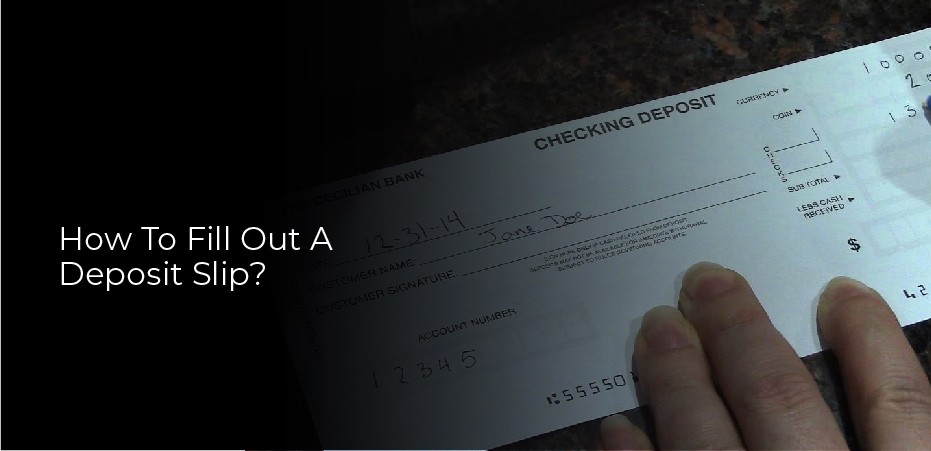

When making a deposit at the bank, you’ll need to fill out a deposit slip. Here’s how to do it:

- Start by filling in your name, address, and account number on the top of the slip.

2. Write the date and amount of the deposit in the appropriate boxes.

3. Indicate what type of deposit it is – cash, check, or money order.

4. List each item being deposited along with the amount of that item.

5. Sign and date the slip when finished.

Check Deposit Details

When you make a deposit at the bank, you likely think that your money is safe. However, there are some things that you need to be aware of when making a deposit. One thing to note is the difference between a check and cash deposit. With a check deposit, the bank will typically place a hold on the funds. This hold can be for a few days or up to two weeks, depending on the bank’s policy.

Another thing to keep in mind is that checks can sometimes bounce. If this happens, the bank may reverse the funds that were deposited and charge you a fee for doing so. In order to avoid this, it’s important to make sure that there are enough funds in your account to cover any checks that you deposit.

Finally, it’s important to keep track of your check deposit history.

Deposits at ATMs

Deposits at ATMs are surging as more people use the machines to put money into their accounts. The number of deposits made at ATMs in the United States totaled $2.27 trillion in 2016, a 5.8 percent increase from 2015, according to data from the Federal Reserve.

The Fed’s data also show that ATM deposits have been growing faster than either checks or transfers, which have both declined in popularity in recent years. In fact, ATM deposits have been increasing every year since 2009, when they totaled $1.57 trillion.

Experts say there are several reasons for the surge in ATM deposits. For one thing, depositing cash is often faster and easier than depositing a check. And with more people using debit cards and mobile payments, there’s less need to deposit checks into a bank account.

Mobile Deposits

Depositing a check used to require a trip to the bank, but now mobile deposits allow you to make the deposit with your phone. This feature is available through most banking apps and allows you to take a picture of the front and back of the check. Once the picture is uploaded, the funds are deposited into your account typically within one business day.

This feature is convenient for people who are on-the-go or live far from a physical bank branch. It can also be helpful if you have a large check to deposit. Mobile deposits typically have no fee, but please check with your specific bank about any applicable charges.

Funds Availability

When you deposit a check, the bank generally credits your account immediately, right? Not necessarily. The term “immediate availability” doesn’t actually mean that the funds are available for withdrawal as soon as the check clears. The bank may place a hold on some or all of the funds, depending on how much money you have in the account, where the check is from, and other factors.

The good news is that federal law limits how long banks can hold your money. If you deposited a check on a Monday, for example, the bank couldn’t hold the funds past Wednesday night. However, if you have an account with a low balance or if the check is from another country, the bank might hold your money for longer.

If you’re not sure how long the bank will hold your funds, call customer service and ask.